python时间序列处理

(1)numpy 中的时间序列

时间类型:numpy.datetime64

创建时间类型变量

import numpy as npx = np.datetime64('2018-12-16')

print(type(x)) # <class 'numpy.datetime64'>

print(x) # 2018-12-16 设置时间型数值的精度

Y 年 M 月 W 周 D 日 h 时 m 分 s 秒

ms 毫秒 us 微秒 ns 纳秒 ps 皮秒 fs 飞秒 as 原秒

import numpy as np# 不设定精度的话就是输入值的精度

print(np.datetime64('2018-12-16 10:31'))

# 2018-12-16T10:31 # 设置精度到秒

print(np.datetime64('2018-12-16', "s"))

# 2018-12-16T00:00:00# 设置精度在毫秒

print(np.datetime64('2018-12-16 12:59:59.50', 'ms'))

# 2018-12-16T12:59:59.500 # 精度到秒,小数部分自动砍掉

print(np.datetime64('2018-12-16 12:59:59.577', 's'))

# 2018-12-16T12:59:59 创建时间型序列,类型用np.datetime64

import numpy as np# 唯一类型 datetime64

date = np.array('2018-12-16', dtype = np.datetime64)

print(type(date)) # <class 'numpy.ndarray'>

print(date) # 2018-12-16data = ['2018-12-16', '2018-12-17', '2018-12-18']

date = np.array(data, dtype = np.datetime64)

print(type(date)) # <class 'numpy.ndarray'>

print(date) # ['2018-12-16' '2018-12-17' '2018-12-18']# 快速生成等步长的时间序列数据

date = np.array('2018-12-16', dtype = np.datetime64)

delta = np.arange(30)

print(date + delta)

'''

['2018-12-16' '2018-12-17' '2018-12-18' '2018-12-19' '2018-12-20''2018-12-21' '2018-12-22' '2018-12-23' '2018-12-24' '2018-12-25''2018-12-26' '2018-12-27' '2018-12-28' '2018-12-29' '2018-12-30''2018-12-31' '2019-01-01' '2019-01-02' '2019-01-03' '2019-01-04''2019-01-05' '2019-01-06' '2019-01-07' '2019-01-08' '2019-01-09''2019-01-10' '2019-01-11' '2019-01-12' '2019-01-13' '2019-01-14']

'''(2)Pandas中的时间序列

以下将会提到四种时间类型:

- 时间戳:表示一个时间点,类型为Timestamp

- 时间增量:两个时间的差,类型为Timedelta

- 时间周期:表示一段时间,类型为Period

- 时间字符串:带时间信息的字符串,类型为str

1.时间戳 Timestamp

①pd.DatetimeIndex():创建时间戳类型的 index

下面是一个例子,创建一个index类型为时间戳序列的df

timeindex = pd.DatetimeIndex(['2014-07-04', '2014-08-04','2015-07-04', '2015-08-04'])

data = pd.Series([3, 1, 5, 4], index = timeindex)

print(data)

# 2014-07-04 3

# 2014-08-04 1

# 2015-07-04 5

# 2015-08-04 4

# dtype: int64print(data['2014-07-04':'2015-07-04'])

# 2014-07-04 3

# 2014-08-04 1

# 2015-07-04 5

# dtype: int64

②时间戳类型index的妙用

timeindex = pd.DatetimeIndex(['2014-07-04', '2014-08-04','2015-07-04', '2015-08-04'])

data = pd.Series([3, 1, 5, 4], index = timeindex)print("特殊取法:根据时间索引值的部分索引")

print(data['2015'])

# 2015-07-04 5

# 2015-08-04 4

# dtype: int64print(data['2015-07'])

# 2015-07-04 5

# dtype: int64③pd.to_datetime():将时间字符串转化为时间戳

Pandas 所有关于日期与时间的处理方法全部都是通过 Timestamp 对象实现的。它利用 numpy.datetime64 的有效存储和向量化接口将 datetime 和 dateutil 的易用性有机结合起来。

import pandas as pd

import numpy as np

from datetime import datetimedate = pd.to_datetime("17th of December, 2018")

print(type(date)) # <class 'pandas._libs.tslibs.timestamps.Timestamp'>

print(date) # 2018-12-17 00:00:00print(pd.to_datetime('2015-Jul-6'))

# 2015-07-06 00:00:00print(pd.to_datetime(['2015-Jul-6', '2015-Jul-6'])) # DatetimeIndex

# DatetimeIndex(['2015-07-06', '2015-07-06'], dtype='datetime64[ns]', freq=None)dates = pd.to_datetime([datetime(2015, 7, 3), '4th of July, 2015','2015-Jul-6', '07-07-2015', '20150708'])

print(dates)

# DatetimeIndex(['2015-07-03', '2015-07-04', '2015-07-06', '2015-07-07',

# '2015-07-08'],

# dtype='datetime64[ns]', freq=None)④datetime.strftime():将时间戳转化为时间字符串

date = pd.to_datetime("17th of December, 2018")

print(date) # 2018-12-17 00:00:00

print(date.strftime('%A')) # Monday

print(date.strftime('%Y-%m-%d')) # 2018-12-17

print(date.strftime('%Y#%m#%d')) # 2018#12#17

关于不同格式的含义可以参考这篇文章结尾那里:python中的时间模块-CSDN博客

2.时间增量 timedelta

①pd.to_timedelta(序列对象, 时间单位):生成时间增量

第二个参数时间单位是用来设置精度的,前面numpy时间序列那里有讲过。

import pandas as pd

import numpy as npdelta1 = pd.to_timedelta(np.arange(12), 'D')

delta2 = pd.to_timedelta([1, 2, 3, 4], 'D')

print(delta1)

# TimedeltaIndex([ '0 days', '1 days', '2 days', '3 days', '4 days',

# '5 days', '6 days', '7 days', '8 days', '9 days',

# '10 days', '11 days'],

# dtype='timedelta64[ns]', freq=None)print(delta2)

# TimedeltaIndex(['1 days', '2 days', '3 days', '4 days'], dtype='timedelta64[ns]', freq=None)②用"时间戳+时间增量"生成多个时间戳

date = pd.to_datetime("17th of December, 2018")

delta = pd.to_timedelta(np.arange(12), 'D')

print(date + delta)# DatetimeIndex(['2018-12-17', '2018-12-18', '2018-12-19', '2018-12-20',

# '2018-12-21', '2018-12-22', '2018-12-23', '2018-12-24',

# '2018-12-25', '2018-12-26', '2018-12-27', '2018-12-28'],

# dtype='datetime64[ns]', freq=None)

③通过两个时间戳相减得到时间增量

dates = pd.to_datetime([datetime(2015, 7, 3), '4th of July, 2015','2015-Jul-6', '07-07-2015', '20150708'])

print(dates)

# DatetimeIndex(['2015-07-03', '2015-07-04', '2015-07-06', '2015-07-07',

# '2015-07-08'],

# dtype='datetime64[ns]', freq=None)print(dates[0])

# 2015-07-03 00:00:00print(dates - dates[0])

# TimedeltaIndex(['0 days', '1 days', '3 days', '4 days', '5 days'], dtype='timedelta64[ns]', freq=None)3.一段时期 Period

Period:时间周期,表示一段时期

①pd.Period():时间戳变为时间周期

import pandas as pdprint("\n①不指定频率时,则默认用当前精度这段时间")

print("比如下面2021就表示2021年年初到2021年年末")

year = pd.Period('2021')

print( 'Start Time:', year.start_time) # 2021-01-01 00:00:00

print( 'End Time:', year.end_time) # 2021-12-31 23:59:59.999999999print("\n再比如2021-02就表示2021年2月月初到2021年2月月末")

year = pd.Period('2021-02')

print( 'Start Time:', year.start_time) # 2021-01-01 00:00:00

print( 'End Time:', year.end_time) # 2021-12-31 23:59:59.999999999print("\n②使用 freq 参数显式指定周期的频率")

print("这里用天,就表示一天的时期")

print("自动变为所给日期的当天,若未给天的日期,则为当月 1 号")

day = pd.Period( '2022-01', freq= 'D')

print( 'Start Time:', day.start_time) # 2022-01-01 00:00:00

print( 'End Time:', day.end_time) # 2022-01-01 23:59:59.999999999day = pd.Period( '2022-01-02', freq= 'D')

print( 'Start Time:', day.start_time) # 2022-01-02 00:00:00

print( 'End Time:', day.end_time) # 2022-01-02 23:59:59.999999999②to_period():将时间戳序列变为时间周期序列

import pandas as pd

import numpy as np

from datetime import datetimedates = pd.to_datetime([datetime(2015, 7, 3), '4th of July, 2015', '2015-Jul-6', '07-07-2015', '20150708'])

print(dates)

print(type(dates[0])) # 时间戳 Timestampper_arr = dates.to_period('M')

print(per_arr)

# PeriodIndex(['2015-07', '2015-07', '2015-07', '2015-07', '2015-07'], dtype='period[M]', freq='M')

print(type(per_arr[0])) # 时间周期 Period

print(per_arr[0])

print(per_arr[0].start_time)

print(per_arr[0].end_time)

③时间周期与标量进行运算,得到新的时间周期

hour = pd.Period( '2022-02-09 16:00:00', freq= 'H')

x = hour + 2

y = hour - 2

print(type(x)) # <class 'pandas._libs.tslibs.period.Period'>

print(x) # 2022-02-09 18:00

print(y) # 2022-02-09 14:00delta = np.arange(10)

result = hour + delta

print(type(result)) # <class 'numpy.ndarray'>

print(result)

# [Period('2022-02-09 16:00', 'H') Period('2022-02-09 17:00', 'H')

# Period('2022-02-09 18:00', 'H') Period('2022-02-09 19:00', 'H')

# Period('2022-02-09 20:00', 'H') Period('2022-02-09 21:00', 'H')

# Period('2022-02-09 22:00', 'H') Period('2022-02-09 23:00', 'H')

# Period('2022-02-10 00:00', 'H') Period('2022-02-10 01:00', 'H')]4.批量生成多个时间戳/时间周期/时间增量

pd.date_range()

例子1:生成多个天的日期序列

# help(pd.date_range)

# date_range(start=None, end=None, periods=None, freq=None, tz=None, normalize=False, name=None, closed=None)print(pd.date_range('2015-07-03', '2015-07-10'))

# DatetimeIndex(['2015-07-03', '2015-07-04', '2015-07-05', '2015-07-06',

# '2015-07-07', '2015-07-08', '2015-07-09', '2015-07-10'],

# dtype='datetime64[ns]', freq='D')print(pd.date_range('2015-07-03', periods = 8))

# DatetimeIndex(['2015-07-03', '2015-07-04', '2015-07-05', '2015-07-06',

# '2015-07-07', '2015-07-08', '2015-07-09', '2015-07-10'],

# dtype='datetime64[ns]', freq='D')print(pd.date_range('2015-07-03', periods = 8, freq = 'H'))

# DatetimeIndex(['2015-07-03 00:00:00', '2015-07-03 01:00:00',

# '2015-07-03 02:00:00', '2015-07-03 03:00:00',

# '2015-07-03 04:00:00', '2015-07-03 05:00:00',

# '2015-07-03 06:00:00', '2015-07-03 07:00:00'],

# dtype='datetime64[ns]', freq='H')例子2:生成多个年末最后一天的时间序列

import pandas as pd

from pandas.tseries.offsets import *dates = pd.date_range('2015-07-01', periods=10, freq = BYearEnd())

# freq参数 按年末(最后一个工作日)生成多个时间戳

print(dates)

# DatetimeIndex(['2015-12-31', '2016-12-30', '2017-12-29', '2018-12-31',

# '2019-12-31', '2020-12-31', '2021-12-31', '2022-12-30',

# '2023-12-29', '2024-12-31'],

# dtype='datetime64[ns]', freq='BA-DEC')

pd.period_range()

例子:生成多个季节周期

# period_range(start=None, end=None, periods=None, freq=None, name=None)

print(pd.period_range('2015-07', periods = 8, freq = 'Q'))# PeriodIndex(['2015Q3', '2015Q4', '2016Q1', '2016Q2', '2016Q3', '2016Q4',

# '2017Q1', '2017Q2'],

# dtype='period[Q-DEC]', freq='Q-DEC')pd.timedelta_range()

例子:生成按小时递增的时间增量

# timedelta_range(start=None, end=None, periods=None, freq=None, name=None, closed=None)print(pd.timedelta_range(0, periods=24, freq='H'))

# TimedeltaIndex(['00:00:00', '01:00:00', '02:00:00', '03:00:00', '04:00:00',

# '05:00:00', '06:00:00', '07:00:00', '08:00:00', '09:00:00',

# '10:00:00', '11:00:00', '12:00:00', '13:00:00', '14:00:00',

# '15:00:00', '16:00:00', '17:00:00', '18:00:00', '19:00:00',

# '20:00:00', '21:00:00', '22:00:00', '23:00:00'],

# dtype='timedelta64[ns]', freq='H')

5.时间频率参数 freq

查看所有的频率类型

import pandas as pd

from pandas.tseries.offsets import *for offset in dir(pd.tseries.offsets):print(offset)频率解释

例子使用理解

print(pd.timedelta_range(0, periods = 20, freq = "2H30T")) # 时间频率为 2 小时 30 分钟

# TimedeltaIndex(['0 days 00:00:00', '0 days 02:30:00', '0 days 05:00:00',

# '0 days 07:30:00', '0 days 10:00:00', '0 days 12:30:00',

# '0 days 15:00:00', '0 days 17:30:00', '0 days 20:00:00',

# '0 days 22:30:00', '1 days 01:00:00', '1 days 03:30:00',

# '1 days 06:00:00', '1 days 08:30:00', '1 days 11:00:00',

# '1 days 13:30:00', '1 days 16:00:00', '1 days 18:30:00',

# '1 days 21:00:00', '1 days 23:30:00'],

# dtype='timedelta64[ns]', freq='150T')print(pd.date_range('2015-07-03', periods = 8, freq = 'BA'))

# DatetimeIndex(['2015-12-31', '2016-12-30', '2017-12-29', '2018-12-31',

# '2019-12-31', '2020-12-31', '2021-12-31', '2022-12-30'],

# dtype='datetime64[ns]', freq='BA-DEC')6.时间分组 df.resample()和 df.asfreq()

这两个方法都是对时间序列进行分组,比如我们有12天的12条数据,现在我们按3天一组,就可以得到4组数据,然后对每个组进行统计啥的。

那这个两个方法的区别是啥,

- resample() : 将每个组的全部数据取出来

- asfreq() : 只取每个组的端点时间

例子1:resample()使用

import pandas as pd

import numpy as np# 生成时间索引,频率T是分钟

ts_index = pd.date_range('2018-08-03', periods=12, freq='T')

ts = pd.Series(np.arange(12), index=ts_index)

print("\n", ts)

'''

2018-08-03 00:00:00 0

2018-08-03 00:01:00 1

2018-08-03 00:02:00 2

2018-08-03 00:03:00 3

2018-08-03 00:04:00 4

2018-08-03 00:05:00 5

2018-08-03 00:06:00 6

2018-08-03 00:07:00 7

2018-08-03 00:08:00 8

2018-08-03 00:09:00 9

2018-08-03 00:10:00 10

2018-08-03 00:11:00 11

Freq: T, dtype: int32

'''# print("\n", ts.resample('5min'))# 按5分钟级别进行时间分组,然后对每个组求和

# 区间默认是左闭右开,比如这里前5分钟是[00:00:00, 00:05:00)

print("\n", ts.resample('5min').sum())

'''

2018-08-03 00:00:00 10

2018-08-03 00:05:00 35

2018-08-03 00:10:00 21

Freq: 5T, dtype: int32

'''# 使用参数closed='right’可以使得区间右端也可以取到

print("\n", ts.resample('5min', closed='right').sum())

'''

2018-08-02 23:55:00 0

2018-08-03 00:00:00 15

2018-08-03 00:05:00 40

2018-08-03 00:10:00 11

Freq: 5T, dtype: int32

'''

例子2:asfreq()使用

print(ts.asfreq('5min'))'''

2018-08-03 00:00:00 0

2018-08-03 00:05:00 5

2018-08-03 00:10:00 10

Freq: 5T, dtype: int32

'''#help(ts.asfreq)例子3:股票数据处理

①加载数据

import pandas as pd

import tushare as ts%matplotlib inline

import matplotlib.pyplot as plt

import seaborn; seaborn.set()# 获取某只股票的交易数据(DataFrame)

stock = ts.get_k_data(code='600547',start='2020', end='2023')

#本接口即将停止更新,请尽快使用Pro版接口:https://waditu.com/document/2

print(stock.head())

# date open close high low volume code

# 0 2020-01-02 22.907 23.329 23.371 22.871 489106.0 600547

# 1 2020-01-03 23.550 24.671 25.007 23.471 987248.0 600547

# 2 2020-01-06 25.900 26.907 26.950 25.900 1234004.0 600547

# 3 2020-01-07 26.107 26.086 26.307 25.550 707042.0 600547

# 4 2020-01-08 27.693 27.321 27.886 26.350 1326357.0 600547# 将'date'列的数据格式转化为时间戳格式

stock['date'] = pd.to_datetime(stock['date']) # 将 date 列变为行索引

stock.set_index('date', inplace=True) # 数据只要收盘价这一列

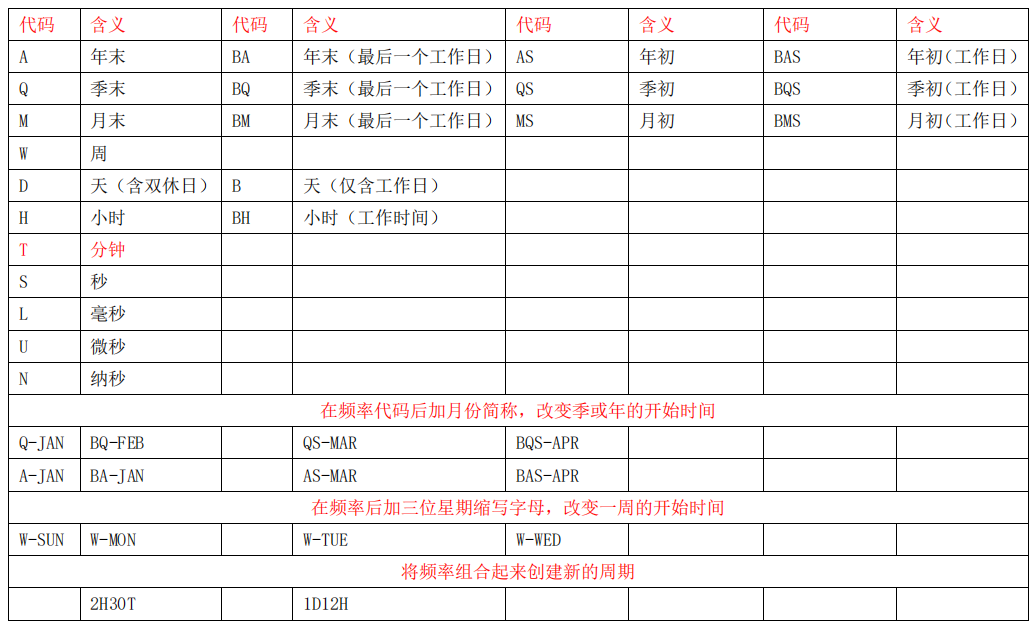

stock = stock['close'] # 画图

plt.plot(stock)

plt.show()

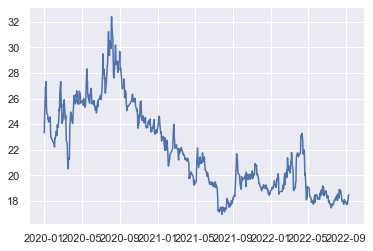

②对年内所有天平均,以及年末最后一天的值

print(list(stock.resample('BA')))

# BA 表示年末(最后一个工作日),这里就是年末到年末之间为一个时间段(一个组)

# 该列表的每个元素是 series,每个 series 表示某一年所有天的数据print(stock.asfreq('BA'))

# 只取了时间段的端点值,这里时间段是年末到年末,所以取的都是年末的值

# date

# 2020-12-31 23.52

# 2021-12-31 18.77

# Freq: BA-DEC, Name: close, dtype: float64# alpha 表示透明度,越接近 0 越透明,越接近 1 越不透明

stock.plot(alpha = 0.5, style = '-') # 统计每一年内的平均值

stock.resample('BA').mean().plot(style = ':') # 统计年末最后一天的值

stock.asfreq('BA').plot(style = '--')# 图例设置

plt.legend(['input', 'resample', 'asfreq'], loc = 'upper center')

plt.show()

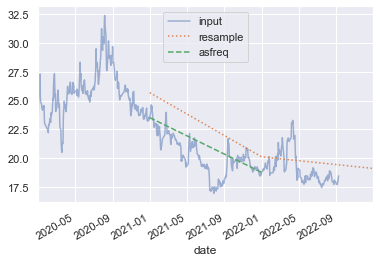

③将缺失值填充为指定值

print(stock.iloc[:10]) # 查看前 10 行可以发现缺失部分日期

'''

date

2020-01-02 23.329

2020-01-03 24.671

2020-01-06 26.907

2020-01-07 26.086

2020-01-08 27.321

2020-01-09 25.350

2020-01-10 24.871

2020-01-13 24.693

2020-01-14 24.393

2020-01-15 24.443

Name: close, dtype: float64

'''# (2,1):2 行 1 列个图形

fig, ax = plt.subplots(2, sharex = True)

data = stock.iloc[:10]# 不填充缺失值画图

data.asfreq('D').plot(ax = ax[0], marker = 'o')# 后向填充缺失值(缺失数据用明天的数据填充)

data.asfreq('D', method = 'bfill').plot(ax = ax[1], style = '-o') # 前向填充缺失值(缺失数据用前一天填充)

data.asfreq('D', method = 'ffill').plot(ax = ax[1], style = '--o')

ax[1].legend(["back-fill", "forward-fill"])

plt.show()

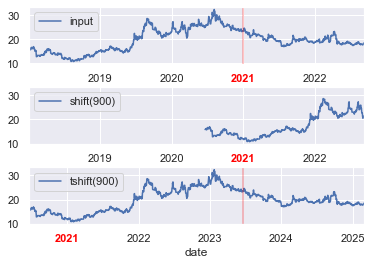

7.日期平移和数据平移

datetimeSeries.shift():平移数据

datetimeSeries.tshift():平移索引

平移什么意思?比如我们长度为3的时间序列数据,比如下面这样

日期 值

20250101 100

20250102 5

20250103 31现在我们将日期这一列平移一天,同时值这一列不动,就变成了这样

日期 值

20250102 100

20250103 5

20250104 31这就是对日期进行平移。

平移有什么用?明显做差分可以用到,当然也还有其它用处,算移动平均啥的。

例子1:用法示例

import pandas as pd

import tushare as ts# % matplotlib inline

import matplotlib.pyplot as plt

import seabornseaborn.set()# 获取某只股票的交易数据(DataFrame)

stock = ts.get_k_data(code='600547', start='2018', end='2023')# 将date列的数据格式转化为时间戳格式

stock['date'] = pd.to_datetime(stock['date'])# 将 date 列变为行索引

stock.set_index('date', inplace=True)# 只取收盘价

stock = stock['close']# 准备3个子图画图,(3,1)个图形 # 共享 y 轴

fig, ax = plt.subplots(3, sharey=True) #

fig.subplots_adjust(hspace=0.4, wspace=0.4)# 对数据应用时间频率,pad 也表示前向填充

stock = stock.asfreq('D', method='pad') # 画图两种方式:ax[0].plot(x,y) data.plot(ax = ax[0])

stock.plot(ax=ax[0]) # 平移数据

stock.shift(900).plot(ax=ax[1]) # 平移索引

stock.tshift(900).plot(ax=ax[2]) # 设置图例与标签

local_max = pd.to_datetime('2021-01-01')

offset = pd.Timedelta(900, 'D')ax[0].legend(['input'], loc=2)

# 将 x 轴第 4 个标签值加粗,红色

ax[0].get_xticklabels()[3].set(weight='heavy', color='red')

# 画垂直的竖线 第一个参数是 x = 某个 xlabel

ax[0].axvline(local_max, alpha=0.3, color='red') ax[1].legend(['shift(900)'], loc=2)

ax[1].get_xticklabels()[3].set(weight='heavy', color='red')

ax[1].axvline(local_max + offset, alpha=0.3, color='red')ax[2].legend(['tshift(900)'], loc=2)

ax[2].get_xticklabels()[1].set(weight='heavy', color='red')

ax[2].axvline(local_max + offset, alpha=0.3, color='red')plt.show() # 显示图像

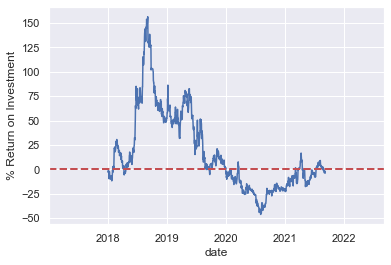

例子2:计算投资回报率

ROI = 100 * (stock.tshift(-365) / stock - 1)

# 比值是明年与今年同期比较

# 横坐标为今年

ROI.plot()

plt.ylabel('% Return on Investment')

plt.axhline(y = 0, c = 'r', ls = '--', lw = 2) # 设置水平参考线 # 注意结尾这个分号的作用

plt.show()

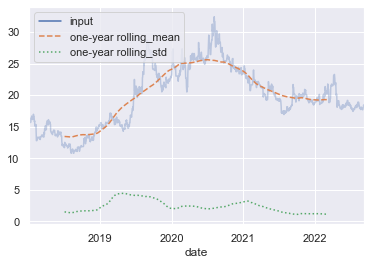

8.移动分组与统计

datetimeSeries.rolling(days, center = True):移动分组,比如可以移动分组后对每组求平均,就得到了移动平均

- 无 center 参数时,取前 days 天的数据为轴 0 的一个组;前面数据量小于 days 的,为空

- 有 center 时,以当前位置为中心,向左右平均取共 days 个数据的平均

例子

print(stock.head(10)) # # 可以看到是从 2018-01-02 开始的

'''

date

2018-01-02 15.818

2018-01-03 15.854

2018-01-04 15.824

2018-01-05 16.022

2018-01-06 16.022

2018-01-07 16.022

2018-01-08 16.237

2018-01-09 15.987

2018-01-10 15.660

2018-01-11 15.829

Freq: D, Name: close, dtype: float64

'''# 移动分组

rolling = stock.rolling(5)

# print(rolling) # Rolling [window=5,center=False,axis=0]

print(rolling.mean()[:10])

'''

date

2018-01-02 NaN

2018-01-03 NaN

2018-01-04 NaN

2018-01-05 NaN

2018-01-06 15.9080

2018-01-07 15.9488

2018-01-08 16.0254

2018-01-09 16.0580

2018-01-10 15.9856

2018-01-11 15.9470

Freq: D, Name: close, dtype: float64

'''rolling = stock.rolling(5, center=True)

print(rolling.mean()[:10])

'''

date

2018-01-02 NaN

2018-01-03 NaN

2018-01-04 15.9080

2018-01-05 15.9488

2018-01-06 16.0254

2018-01-07 16.0580

2018-01-08 15.9856

2018-01-09 15.9470

2018-01-10 16.0114

2018-01-11 16.0328

Freq: D, Name: close, dtype: float64

'''# rolling.mean()和 rolling.std()

rolling = stock.rolling(365, center=True)

data = pd.DataFrame({'input': stock,'one-year rolling_mean': rolling.mean(),'one-year rolling_std': rolling.std()})

ax = data.plot(style=['-', '--', ':'])

ax.lines[0].set_alpha(0.3)

end